By Colin Lloyd

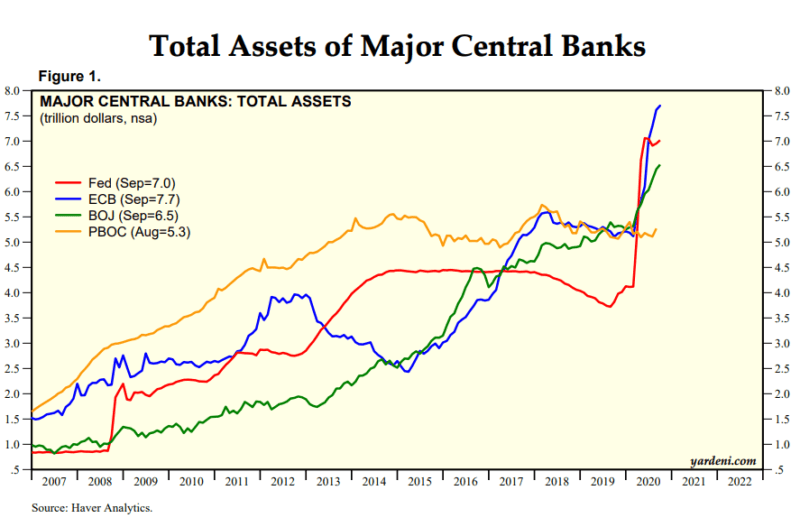

The original experiment in quantitative easing (QE) began in Japan on the 20th of March 2001, although the Bank of Japan (BoJ) had already been wrestling with the wisdom of embracing QE for several years. By the time of the great financial crisis in 2008/09, the Japanese experiment had attracted several additional adherents. The chart below shows how the balance sheets of the major central banks have grown since then:

Source: Yardeni, Haver Analytics

The BoJ remains in the vanguard of policy initiatives, moving seamlessly on from radical QE to ultra-radical QQE – quantitative and qualitative easing. Armed with this new weapon they have embarked on the provision of, not just temporary liquidity by the purchase of government and corporate bonds, but also, permanent capital, via the acquisition of exchange traded funds of Japanese common stocks. By the spring of this year the BoJ was acknowledged to be the largest holder of Japanese corporate shares.

Where the BoJ leads, other central banks will follow. Interest rates may be at the zero bound, the government bond yield curve flat and corporate bond yield spreads near historic lows, but the central banks still have plenty of firepower in pursuit of their cherished inflation targets and full employment. Given the global seismic impact of the pandemic which has engulfed the planet, this is a great relief to many world leaders, but now monetary stimulus must go further; it must go global.

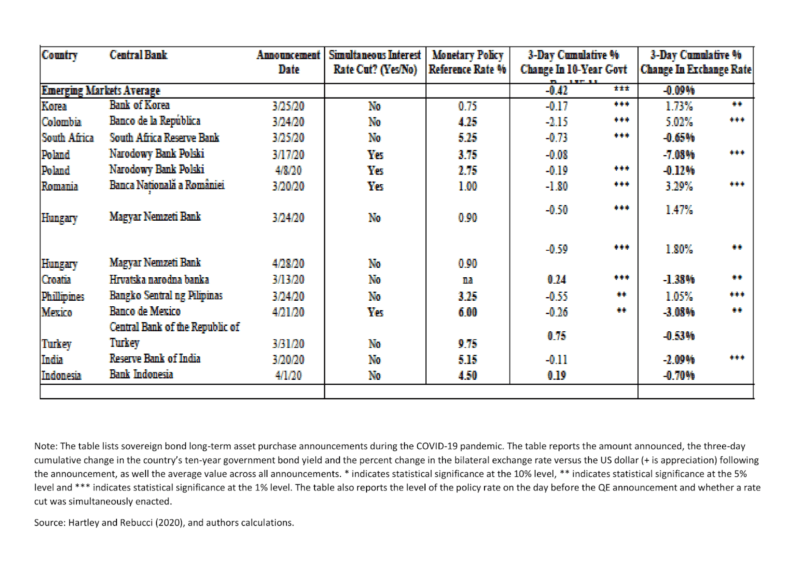

The table below shows the wide array of central banks which have resorted to bond purchases since March and the initial impact this had on both their government bond yields and their currencies.

Source: VoxEU CEPR, Hartley and Rebucci

Become an Activist Post Patron for $1 per month at Patreon.

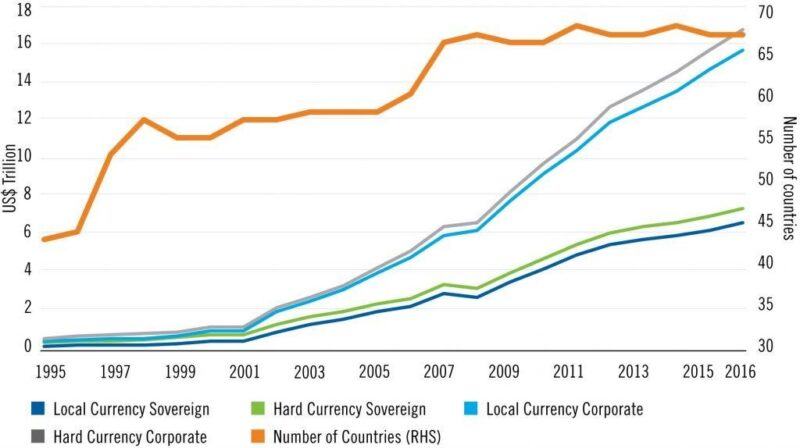

In part, the reason that these bond market interventions have been possible, without a precipitous decline in their currencies, is due to the much larger percentage of local currency bonds issued. The risks laid bare by the Asian crisis of 1997 prompted many nations to rethink their capital raising techniques:

Source: FT, Institute of International Finance

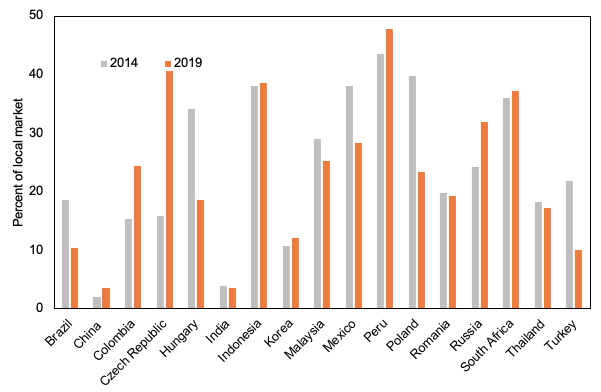

It has been generally accepted by global financial markets that unorthodox policies, such as zero interest rates and QE, favour large, industrialised, globally integrated economies with reasonably open borders and free-trade policies. For smaller, less developed nations the risks remain high. The current crisis, which has accelerated so many nascent trends, has also ushered in a new era where a credible Emerging Market (EM) country, with a flexible exchange rate and well-anchored inflation expectations, may now be able to minimise the risk of a large currency depreciation or spiralling inflation. What may be more difficult to absorb is the selling of bonds by international investors in a risk-off environment:

Source: Institute of International Finance

For emerging nations which rely on natural resources, the opportunity for their central banks to embrace unorthodox monetary policy is more limited. As global demand for commodities has waned so prices have fallen, deflationary forces may wreak even greater havoc on the balance of trade. A government’s bonds are only as creditworthy as the stability of its tax base. EM countries that are reliant on tourism will find they face similar challenges. QE will not be the solution to all the world’s ills.

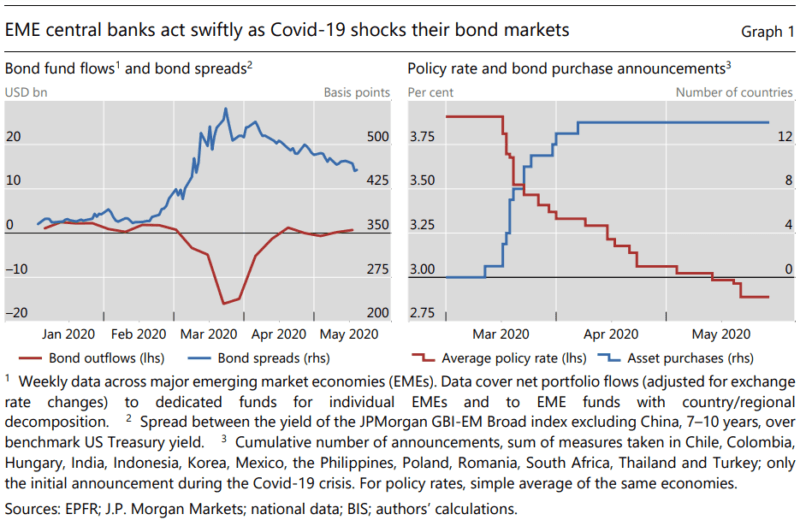

In economic terms, the current pandemic differs from previous sudden stop episodes in that it has simultaneously eroded both supply and demand. Financial markets have paid scant attention to judge by the behaviour of EM government bonds. As in 2008, EM bond yields rose, but the global monetary and fiscal response was swifter, more aggressive and more global. EM and Developed Market (DM) central banks joined forces in a concerted intervention:

Source: BIS, EPFR, JP Morgan

The ameliorating effects of the combination of DM and EM QE has percolated down through bonds to equity markets. As at the end of September, EM equities were within 4% of their pre-pandemic peak.

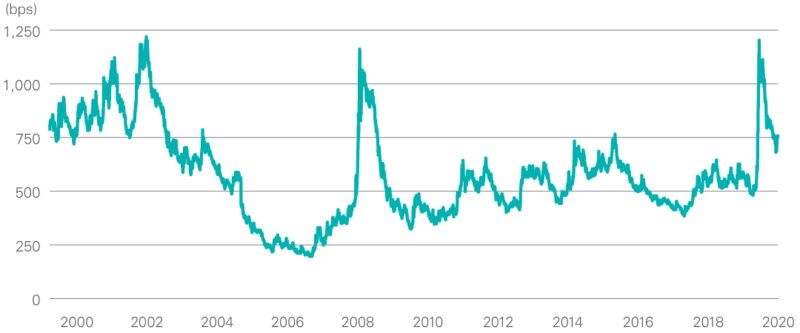

EM debt performance has been more varied in Q3, both across sub-asset classes as well as by country. The modest selloff during the final weeks of the quarter was probably more a result of position squaring than a change in expectations; nonetheless, the strong upward momentum of Q2 is diminished. Looking ahead, the EM country lockdowns of March, April and May have given way to a more targeted approach to stemming the second wave of infections. EM economies remain open for business and government fiscal support is gradually being withdrawn.

This might encourage cautious investors to moderate their purchases, but for yield-hungry investors, High Yield EM debt at around 700bp remains an alluring alternative to US Treasuries:

Source: Lazard Asset Management, JP Morgan

Concerns about EM exchange rate weakness should always be taken seriously, but, after an initial US$ flight to quality during the early stages of the Covid outbreak in March, the performance of EM currencies has been almost as impressive as the performance of their bonds. I would caution, nonetheless, that this strength is more a function of international capital flows as it is central bank accommodation:

Source: Investing.com, MSCI

What are the limits of EM QE?

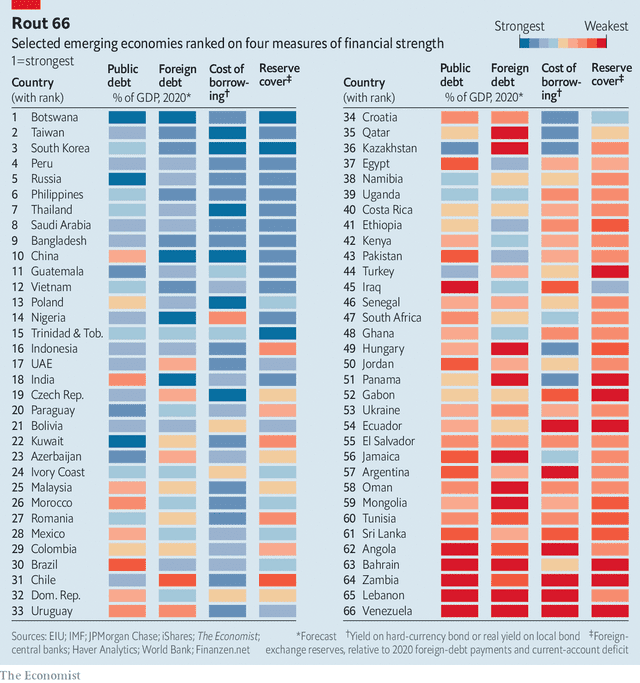

Yield compression between EM and DM bonds is unlikely to abate and yet EM economies remain far from equal. The table below provides a useful ranking of some of those strengths and weaknesses:

Source: The Economist

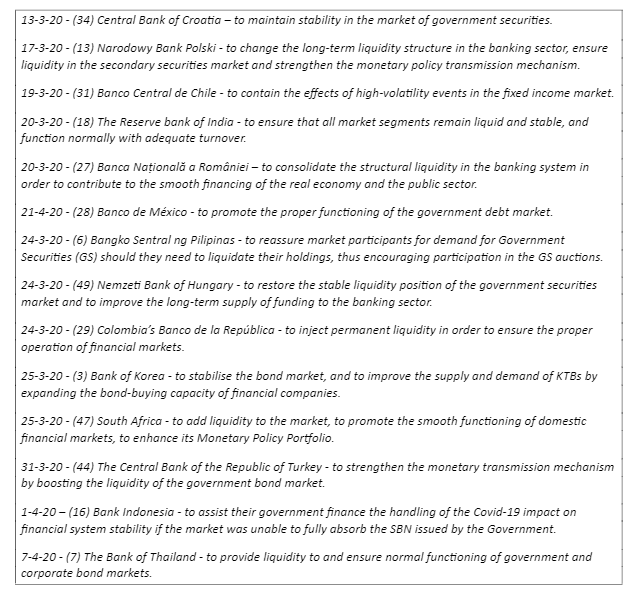

Set against this backdrop the timeline for central bank bond purchases and their justification for the adoption of these programmes was as follows (I have also included their Rout 66 ranking from the table above):

It is interesting to note that despite its relative economic strength, Thailand was slow to follow the lead of other EM central banks – perhaps the long shadow of the Asian crisis stayed its hand a while? Also of interest are the actions of Turkey and South Africa. Both the Turkish Lira and the South African Rand had been under speculative pressure during the previous two years or more. Since the spring, the Rand has rebounded somewhat; the Lira, by contrast, continues to decline.

The scale of EM bond purchases has been moderate thus far, but, as central bankers around the world know, their actions will be scrutinised closely. What are the limits of QE for EM countries? Will economic strength afford sufficient protection from speculators? How important is the level of a central bank’s foreign exchange reserves in this delicate equation? The financial markets will seek to discover by testing their mettle.

The table at the beginning of this article, if ranked by economic strength, leaves many questions as to the limits of EM QE. Croatia, for example, which led the way on the 13th of March, saw bond yields rise and their currency decline. Their Rout 66 rank (34) was fairly low so this may have been predictable, yet Hungary (rank 49) saw yields decline 59bp and the Forint rose 1.8%.

The latest incarnation of unorthodox monetary policy is young. In a fiat currency world the limits of central bank balance sheet expansion remain unclear, but, as the world economy recovers from the largest economic shock in generations, those limits will become clear. For the large, DM, central banks, these EM limits will be noted with care. Japan has been the petri dish of global monetary policy for the last two decades; now it is the turn of EM central banks to test the willing suspension of disbelief of global financial markets.

Source: AIER.org

Colin is a macroeconomic commentator, writer and presenter, based in London, England. He has worked for asset managers in commodities, money markets, capital markets, equities and foreign exchange since the early 1980’s and writes In the Long Run. He is a contributor to several free-market publications including The Cobden Centre and was a 2017 runner-up for the 2017 Richard Koch Breakthrough Prize awarded by The Institute of Economic Affairs.