By Pam Martens and Russ Martens:

President Joe Biden is putting the national security of the United States at risk by not suspending the short-selling of federally-insured banks. Concerns over the safety and soundness of the U.S. financial system could cause money flight out of the U.S., impacting the strength of the U.S. dollar and a loss of confidence by our foreign allies.

This is also a matter that impacts the financial lives of every American, because every American – rich, poor or middle class – will suffer the consequences in terms of ability to access bank credit and higher fees on that credit as a result of rebuilding the rapidly depleting federal Deposit Insurance Fund that protects bank deposits.

The second, third and fourth largest bank failures in the history of the U.S. have now occurred in the span of seven weeks (First Republic Bank, Silicon Valley Bank and Signature Bank, respectively) with the Federal Deposit Insurance Corporation (FDIC) taking big hits in each case to its Deposit Insurance Fund.

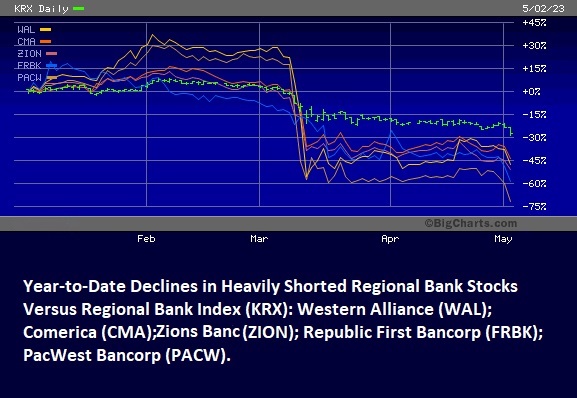

At the time of First Republic Bank’s failure on Monday (with JPMorgan Chase given a very sweet deal by the FDIC to buy its underwater assets and take over the deposits that hadn’t yet fled), it was one of the most heavily shorted bank stocks with one-third of its outstanding shares shorted as of one week before it failed, according to a report from Reuters.

First Republic Bank was not a small bank. At the time of its demise, it had $207.5 billion in assets. According to a statement from the FDIC on Monday, it “estimates that the cost to the Deposit Insurance Fund will be about $13 billion. This is an estimate and the final cost will be determined when the FDIC terminates the receivership.”

The FDIC estimated the cost to the Deposit Insurance Fund in the failure of Silicon Valley Bank to be $20 billion, and the cost to the DIF in the failure of Signature Bank to be $2.5 billion.